All Categories

Featured

Table of Contents

A PUAR permits you to "overfund" your insurance coverage right approximately line of it ending up being a Customized Endowment Contract (MEC). When you use a PUAR, you rapidly raise your cash money value (and your survivor benefit), thereby boosting the power of your "bank". Additionally, the even more cash value you have, the better your interest and returns settlements from your insurance provider will be.

With the surge of TikTok as an information-sharing platform, financial guidance and approaches have located an unique means of dispersing. One such approach that has actually been making the rounds is the unlimited banking idea, or IBC for short, garnering endorsements from celebrities like rap artist Waka Flocka Fire. Nonetheless, while the method is presently prominent, its origins trace back to the 1980s when economic expert Nelson Nash introduced it to the world.

How do I optimize my cash flow with Cash Value Leveraging?

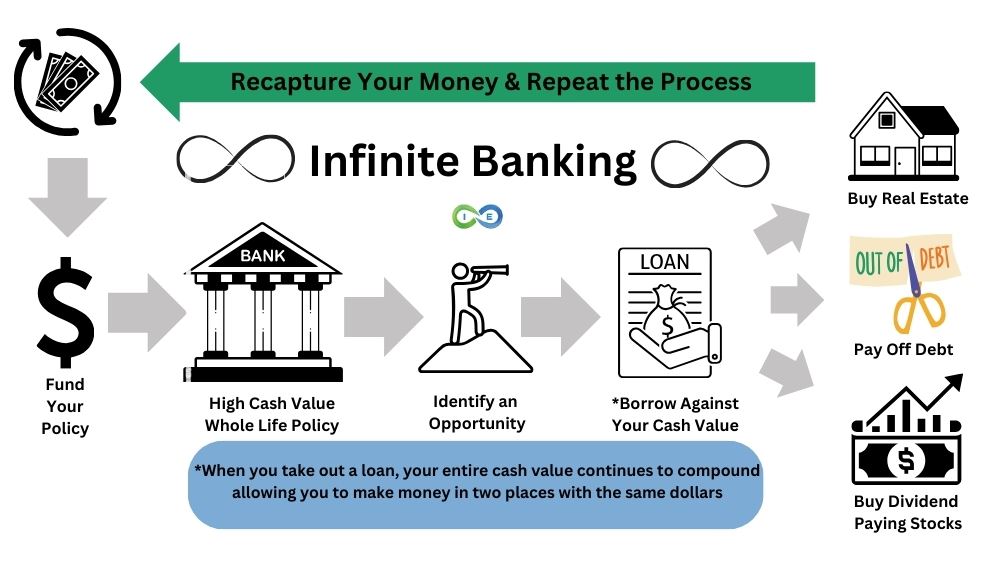

Within these plans, the cash worth grows based upon a price set by the insurance company (Whole life for Infinite Banking). As soon as a significant money worth gathers, insurance holders can acquire a money value funding. These lendings vary from traditional ones, with life insurance policy offering as collateral, implying one might shed their protection if loaning exceedingly without adequate cash money value to support the insurance policy expenses

And while the appeal of these policies appears, there are innate limitations and threats, demanding persistent cash worth monitoring. The strategy's authenticity isn't black and white. For high-net-worth people or company owner, particularly those making use of approaches like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance growth might be appealing.

The attraction of boundless financial doesn't negate its obstacles: Expense: The fundamental need, a permanent life insurance policy, is more expensive than its term equivalents. Qualification: Not everybody gets approved for entire life insurance policy because of rigorous underwriting procedures that can exclude those with particular health and wellness or way of living conditions. Intricacy and danger: The intricate nature of IBC, paired with its dangers, may hinder numerous, especially when easier and less high-risk choices are available.

How do I optimize my cash flow with Borrowing Against Cash Value?

Designating around 10% of your monthly revenue to the policy is simply not viable for lots of people. Utilizing life insurance policy as an investment and liquidity source calls for discipline and surveillance of policy cash worth. Get in touch with a monetary consultant to determine if limitless banking lines up with your priorities. Part of what you review below is simply a reiteration of what has actually already been said above.

So before you obtain right into a scenario you're not planned for, know the adhering to first: Although the concept is frequently sold thus, you're not in fact taking a funding from yourself. If that held true, you wouldn't have to settle it. Rather, you're borrowing from the insurance business and have to repay it with interest.

Some social media messages advise making use of money value from whole life insurance coverage to pay down credit history card financial obligation. When you pay back the car loan, a part of that rate of interest goes to the insurance coverage company.

For the initial several years, you'll be paying off the commission. This makes it exceptionally hard for your policy to build up worth throughout this time. Unless you can pay for to pay a few to several hundred bucks for the following years or more, IBC will not function for you.

Infinite Banking Benefits

Not everyone should rely entirely on themselves for financial protection. If you need life insurance policy, here are some beneficial pointers to consider: Think about term life insurance policy. These policies give protection throughout years with significant monetary obligations, like mortgages, student finances, or when taking care of young kids. See to it to look around for the very best price.

Picture never having to worry regarding financial institution loans or high interest prices once again. That's the power of unlimited banking life insurance.

There's no collection car loan term, and you have the flexibility to decide on the payment schedule, which can be as leisurely as repaying the financing at the time of death. Infinite Banking cash flow. This versatility expands to the servicing of the car loans, where you can go with interest-only repayments, maintaining the loan equilibrium flat and workable

Holding money in an IUL dealt with account being credited passion can often be far better than holding the money on down payment at a bank.: You've always imagined opening your very own bakeshop. You can obtain from your IUL policy to cover the preliminary expenditures of renting out a space, acquiring devices, and employing staff.

Cash Value Leveraging

Individual finances can be acquired from traditional financial institutions and credit history unions. Borrowing cash on a debt card is usually really pricey with annual portion prices of rate of interest (APR) typically reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Infinite Banking Toolkit

Borrowing Against Whole Life Insurance

Infinite Income System